December 2022 – Week 4 Edition

Gold Hits a Six-Month High

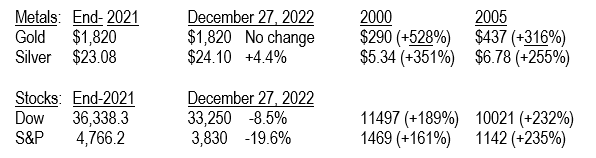

Gold reached a six-month high above $1,830 an ounce Tuesday morning, December 27, based on a weaker dollar and rising crude oil prices. Silver rose $0.40 in sympathy to $24.30 before settling back. Silver should close the year in positive territory with gold on the cusp of breaking even, with a chance to remain positive as well. Gold is already up double-digits in many major currencies, including the British pound and Japanese yen. Next week, we’ll bring you a year-end summary but the metals are clearly beating the stock market. The U.S. Dollar Index fell from 113 to 104 (-8%) in November and December, fueling the metals’ rise.

Congress Passes Huge Spending Bill While Rates Are Soaring – A Recipe for Catastrophe

Everybody is talking about the Fed raising rates but nobody I can see is talking about the HUGE impact this will have on the budget deficit in future years. The Fed is not only raising rates to 4.5%, and soon to over 5% but they are talking about leaving rates that high for years to come. What will that do to our budget deficits when the average Treasury bond is more like 5% than 1% to 1.5% – especially when the cumulative federal debt grows from $21 trillion in 2019 to $31 trillion (now) and $41 trillion in 2026?

Amazingly, Congress passed a new $1.7 trillion spending bill last Friday, which will probably cost well over $2 trillion when all the pork is added in the New Year, pushing the deficit ever higher. This bill was passed just 11 days before a new Republican majority would take over the House of Representatives and amazingly a handful of Republicans in the House and Senate voted for it, probably because it contained tons of special interest spending for a variety of Republican districts, as well as Democrats.

The federal debt totaled $31.4 trillion as of November 30, 2022, according to the U.S. Treasury, doubling in the last decade. Back in May, when the average Treasury rates were much lower, the Congressional Budget Office (CBO) projected the annual net interest costs would total about $400 billion in 2022 (1.3% interest on $31.4 trillion). They forecasted this debt load would nearly triple over the next decade, soaring to $1.2 trillion annually, adding up to over $8 trillion in the next 10 years. But bear in mind this CBO forecast was drafted back in May, when interest rates were much lower than they are today.

Look at what has happened since last May. The Fed has raised rates seven times this year to 4.5% and the Treasury must hold auctions for new debt by issuing 1-to-3-year Treasury Bills and Notes. The average rate on these securities is now around 4.5%. Simple math says that 4.5% of $31.4 trillion is $1.4 trillion, a debt service figure the CBO said last May we weren’t supposed to see until the mid-2030s! And now, Congress is adding new debt, so the debt service on $41 trillion in 2026 at 5% will be over $2 trillion per year, or about one-third of the current federal budget. That’s far more than the projected defense budget.

According to the CBO’s model, interest payments could exceed $66 trillion over the next 30 years, absorbing nearly 40% of all federal revenues by 2052 and becoming the largest federal expenditure, exceeding defense spending before 2030, Medicare by 2046 and Social Security by 2049.

The current U.S. debt/GDP ratio is about 120%, a level we only saw one other time in our history, briefly, at the end of World War II, after fighting two world wars on two fronts – Europe and the Pacific. Today, the relevant model is Japan, where the debt-to-GDP ratio is over twice as high, 262%. In Japan, they have not seen meaningful economic growth in over 30 years. That should be a warning to Washington, DC.

The Fed and the Treasury created this monster through inflation, which they decried as being “transitory.”

Fed Chair Jerome Powell and Secretary of the Treasury Janet Yellen said the “T” word, and everyone followed:

“All of the economists that the President has been relying on suggest there is a transitory nature to

the inflation problem.” --Jennifer Granholm, U.S. Secretary of Energy, November 27, 2021

“This inflation that we’re experiencing is transitory. It is not going to be here for long.”

--Representative Maxine Waters (D-Cal), November 28, 2021

Then the Fed finally attacked inflation in 2022 with monstrous interest rate increases, which could destroy our economy and cripple our growth prospects for years to come. The Japanese yen has been weak for years due to its high debt-to-GDP ratio – a similar trend in the U.S. could decimate our currency. The one positive takeaway is that economic stress and high inflation are usually very bullish for gold.

CNBC Panel Debates $4,000 Gold in 2023

We’ve already reported how Ole Hanson of Denmark’s Saxo Bank sees $3,000 gold next year, with a potential surge to $4,000. Last week, a CNBC panel held on December 22 debated the fate of gold next year. One panelist, Juerg Kiener, managing director and chief investment officer of Swiss Asia Capital, said gold could surge to $4,000 next year as interest rate hikes and recession fears keep markets volatile.

On CNBC’s Asia-based program, “Street Signs Asia,” Kiener predicted gold would reach a range of between $2,500 and $4,000 next year. He said gold’s move “is not going to be just 10% or 20%,” but a move that will “really make new highs.” He said recessions in the first quarter in many nations will cause a slowdown in rate increases, which will make gold more attractive, especially for central bank buying.

Kiener pointed out that central banks bought 400 metric tons of gold last quarter, almost doubling the 241 tons they bought in the third quarter of 2018. He also pointed out, as we have, that, “Since [the] 2000s, the average return [on] gold in any currency is somewhere between 8% and 10% a year. You haven’t achieved that in the bond market. You have not achieved that in the equity market.” He added, “Gold is a very good inflation hedge, a great catch during stagflation and a great add onto a portfolio.”

A second panelist, Kenny Polcari, senior market strategist at Slatestone Wealth, said “I don’t have a $4,000 price target on it, although I’d love to see it go there.” He said gold’s price would be determined by how inflation responds to interest rate hikes, but added, “I like gold. I’ve always liked gold,” advising investors: “Gold should be a part of your portfolio. I think it is going to do better.”

A third panelist, Nikhil Kamath, co-founder of India’s largest brokerage, Zerodha, said investors should allocate 10% to 20% of their portfolio to gold as a “relevant strategy” going into 2023. “Gold also traditionally has been inversely proportional to inflation, and it has been a good hedge against inflation,” adding that, “If you look at how much gold you require to buy a mean home in the 70s, you probably require the same or lesser amount of gold today than you did back in the 70s, or the 80s, or the 90s.”

We haven’t seen this number of mainstream analysts predict significantly higher gold prices since the start of 2020, which was the last time gold surged to an all-time high of $2,089 on August 6, 2020. I don’t know if gold will reach the $4,000 mark but I agree with the other experts that we should see a significant increase in the price of gold in 2023. My conservative estimate would put it between $2,500 an ounce and just over $3,000 an ounce but it wouldn’t hurt my feelings to see it even higher. That said, now is clearly the time to buy gold. Call your professional account representative today and talk with them about the latest gold forecast and how you could benefit.

Important Disclosure Notification: All statements, opinions, pricing, and ideas herein are believed to be reliable, truthful and accurate to the best of the Publisher's knowledge at this time. They are not guaranteed in any way by anybody and are subject to change over time. The Publisher disclaims and is not liable for any claims or losses which may be incurred by third parties while relying on information published herein. Individuals should not look at this publication as giving finance or investment advice or information for their individual suitability. All readers are advised to independently verify all representations made herein or by its representatives for your individual suitability before making your investment or collecting decisions. Arbitration: This company strives to handle customer complaint issues directly with customer in an expeditious manner. In the event an amicable resolution cannot be reached, you agree to accept binding arbitration. Any dispute, controversy, claim or disagreement arising out of or relating to transactions between you and this company shall be resolved by binding arbitration pursuant to the Federal Arbitration Act and conducted in Beaumont, Jefferson County, Texas. It is understood that the parties waive any right to a jury trial. Judgment upon the award rendered by the Arbitrator may be entered in any court having jurisdiction thereof. Reproduction or quotation of this newsletter is prohibited without written permission of the Publisher.